As compliance professional are aware, continuing professional education (CPE) can be complicated to navigate for accounting and consulting firms, Certified Public Accountants (CPA), and non-CPA firm professionals. Firm CPE compliance professionals are primarily responsible for educating firm leadership and professionals, monitoring and communicating proposed and newly released rule changes, and advising the firm and its professionals of upcoming deadlines and CPE statuses to meet deadlines.

CPAs and Non-CPA professionals are often unaware they must fulfill CPE requirements based on their firm’s professional development requirements, PCAOB, Yellow Book, IRS, or for other industry related regulators. In addition, individuals typically have multiple annual, bi-annual, and triennial requirements which may end mid-year, end of year, birth month, birthday, license anniversary date, or another period as regulator assigned.

Below is an overview of the CPE compliance landscape. We hope you find this information helpful for yourself and in educating others who may be unfamiliar with the complexities.

Primary U.S. CPA Industry Regulators

- State Boards of Accountancy

- Public Company Accounting Oversight Board (PCAOB)

- American Institute of Certified Professional Accountants (AICPA)

- U.S. Government Accountability Office (GAO AKA Yellow Book)

- Internal Revenue Service -Tax Preparers (IRS)

CPE Program Qualification

The AICPA and the National State Board of Accountancy (NASBA) – Registry develop national guidelines for the acceptable development and delivery of qualified CPE training. Additionally, each regulator independently establishes, reviews, and revises acceptable CPE requirements and cycle deadlines as they deem appropriate. Many regulators also require annual sub-requirements be met during multi-year cycles.

CPA Mobility Nuances by State

Around 2014 most State Boards of Accountancy had begun adopting the concept of CPA Mobility which allows CPAs licensed in one state to provide practice services as a CPA in another state without additional licensing based on substantial equivalency. Although CPA Mobility simplified licensing and CPE requirements, there continue to be nuances by-state that firms and professionals must navigate. Following are examples:

- New York CPA licenses are issued for life by The Office of the Professions. CPAs who relocate and obtain a license in a new home state may not be eligible to continue serving New York clients under CPA mobility. Under these circumstances the licensee may be required to maintain an active New York CPA license.

- Effective in 2020 Section 2-109 of the Illinois Human Rights Act (“IHRA”) requires approved annual sexual harassment training for every employer with employees working in the State. This would apply to CPAs licensed in another state who are providing services to Illinois clients.

- Reciprocal licenses in some states require the holder to obtain all or some training regardless of meeting home state CPE requirements. For instance, a District of Columbia licensee holding a reciprocal Florida license is required to meet the Florida ethics requirement to maintain the license.

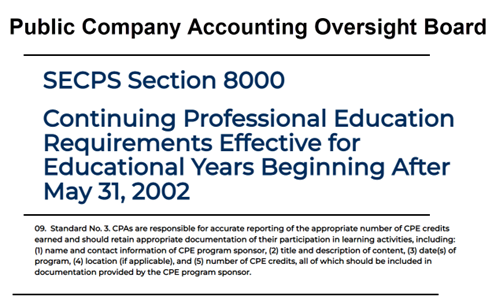

- Non-CPA professionals in a CPA firm may be required to fulfill CPE to meet PCAOB (see .09), GAO (see chapter 4) or a requirement of another regulator or jurisdiction.

LCvista CPE Compliance Management Solution Community

Upcoming CPE rule changes impacting our Compliance Management Solution are monitored by the LCvista CPE Compliance team and by our knowledgeable CPE Compliance administrator community from firms across the country. Updates to jurisdiction rules are released close to effective dates, and clients are notified of changes through weekly release note emails. The entire LCvista CPE Compliance community has cultivated relationships over many years with local and national regulators which allow us to maintain the most current jurisdiction rules and to uniquely support our CPE Compliance administrator community.